Budgeting Grade 12 - Accounting Grade 12 Study Guide and Notes

Share via Whatsapp Join our WhatsApp Group Join our Telegram GroupTable of contents

- How to use this study guide

- Study and examination tips

- Overview of the topic: budgeting

- Unpacking the sections of the budget

4.1 Sales and collections from debtors

4.2 Purchases and payments to creditors

4.3 Unpacking the budget (calculations)

4.4 Analyzing and interpreting budget information - Check your answers

- Message to grade 12 learners from the writers

- Thank you

How to use this study guide

The main intention of this study guide is to address the challenges with specific areas of subject content that was poorly answered in the past nsc papers. This is informed by the detailed question-by-question analysis and findings provided in the diagnostic reports. The material presented in this booklet focuses on the progression across the fet phase and the content overlap, as illustrated in the table below.

| GRADE 12 | GRADE 10/11 (overlap) | |

| Field 1: Financial Accounting | Companies

Reconciliations analysis | Bookkeeping (sole trader/ partnership)

Reconciliations prepare |

| Field 2: Managerial Accounting | Manufacturing concerns

Budgeting (analysis)

| Manufacturing

Budgeting (prepare)

|

| Field 3: Managing Resources | Stock valuation

Fixed asset management(analysis) Auditing, internal controlsand ethics | Stock (clubs)

Fixed assets (prepare)

Auditing, internal controls and ethics |

Grade 12 learners (and teachers) must first address prior knowledge (concepts and calculations), before moving to the more challenging aspects of analyzing, interpreting and commenting. The next logical step is to tackle examination-type questions with the understanding that all questions will make provision for the different cognitive levels.

This study guide provides:

- Explanatory notes comprising simple definitions, examples, formulae and short-cuts (handy hints).

- Short focus-activities to test specific skills and content.

- Application activities in the form of examination-type questions.

- Adapted questions from past examination papers.

Plan of Action:

- You need to master the basic skills by using this manual, together with all other resources such as textbooks and study guides, to obtain more practice

examples. - Test your knowledge by attempting a variety of examination questions.

- Make notes of your shortcomings and start the process again until you are able to get the correct answers to the activities

Study and examination tips

Know the paper: General structure and layout.

- The Accounting paper is one 3-hour paper for 300 marks.

- It consists of 6 compulsory questions; the marks per question range from 30 to 80 marks. Each question comprises a number of sub-questions that catering for the different cognitive levels.

- The content covered must conform to the requirements of CAPS, as follows:

| Financial Accounting | 50% - 60% | 150 - 180 marks |

| Managerial Accounting | 20% - 25% | 60 - 75 marks |

| Managing Resources | 20% - 25% | 60 - 75 marks |

The trend in past papers was as follows:

- Question 1, 2 and 6 are generally shorter questions (30 - 45 marks).

- Question 3 and 4 are generally the longer questions, comprising Financial Statements, the Cash Flow Statement and Interpretation.

- The question paper comes with a specially prepared ANSWER BOOK, with appropriate space, formatting and certain details, which means you can answer the questions in any order.

Strategy:

√ Budgeting forms part of the Managerial Accounting field and, together with Manufacturing, it must constitute 20% - 25% of the paper.

√ Past trends show that the topic is normally assessed in Question 5 or 6 and is 30 - 40 marks; ± 20 marks will require calculations and the balance will be on analysis and interpretation.

√ Examiners will switch between the Cash Budget and the Projected Income Statement. There are subtle differences in interpretation, but the calculations are similar. (Detailed explanations are provided in Section 5 of this document).

√ The calculations require good arithmetical ability, which is developed over a period of time, and starting in Grade 7.

√ These skills must include calculating percentages, increases, decreases or specific amounts using equations.

√ Interpretation requires good comprehension ability. Be mindful of the language of the paper, and practice using many past papers.

Overview of the topic: Budgeting

What are some of the words that come to mind?

Discuss the words that are confusing Piet.

Make a list of other relevant words/ terms that came up in your discussion/ brainstorming session.

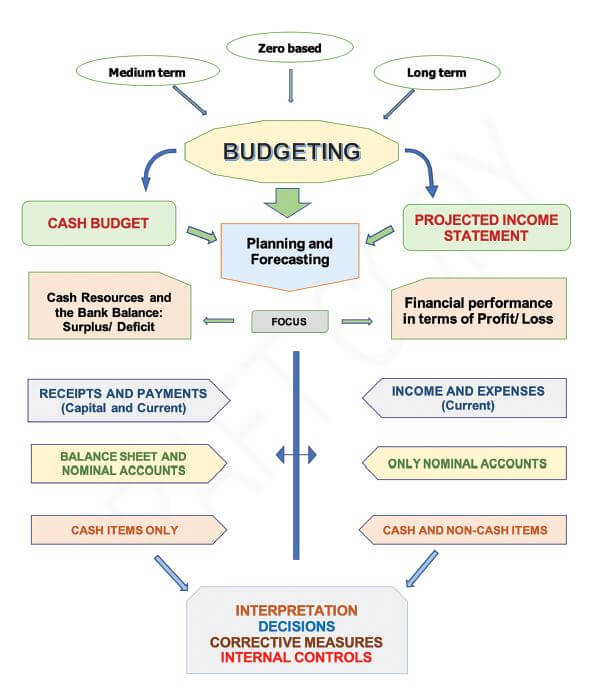

An EXPLANATION that highlights the purpose of budgeting:

Budgeting is an internal control tool that involves projecting business results, using existing

business information as well as other external factors, making adjustments and taking decisions to achieve the objectives of the business.

Summary of the topic:

Start-up Activity: Do I understand the difference between Receipts, Payments, Income and Expenses?

Place the correct amount in the respective column/s. Amounts can apply to more than one column.

| NO | INFORMATION | CASH BUDGET | PROJECTED INCOME STATEMENT | ||

| RECEIPT | PAYMENT | INCOME | EXPENSE | ||

| a | Cash sales are expected to be R7 400 per month at a 25% mark-up on cost. | ||||

| b | An old computer with a carrying value of R4 400 will be sold for R2 500 cash in the next month. | ||||

| c | Depreciation on equipment is estimated to be R950 per month. | ||||

| d | An annual insurance premium of R5 200 is paid by cheque. R1 200 of the payment is for the next financial year. | ||||

What are we expected to cover in Grade 12?

- Back to basics

- Concepts and terminology from previous Grades.

- The difference between the Cash Budget and the Projected Income Statement. o Purpose of preparing a Cash Budget or a Projected Income Statement.

- Arithmetical ability

- Calculate missing amounts in the budget.

- Calculate amount/s for specific items using information from the budget, such as the loan balance or the total cost of a vehicle purchased.

- The answers are usually:

specific amounts, percentages, increases, decreases or ratio relationships.

- The answers are usually:

- Analysis and Interpretation

- Compare Actual vs Budgeted figures:

- Provide possible reasons for differences.

- Provide solutions (internal controls).

- Consider ethical issues in terms of cash management and adherence to the budget.

- Problem solving:

- Control of cash, debtors, creditors, stock

- Business decisions such as buy/rent fixed assets, sales and profitability.

- Compare Actual vs Budgeted figures:

Unpacking the sections of the budget:

4.1 Sales and collection from debtors

EXAMPLE: Cash sales amounts to 30% of total sales.

Calculate the missing amounts.

| TOTAL SALES 100% | CASH SALES 30% | CREDIT SALES 70% | |

| March | 320 000 | 96 000 | 224 000 |

| April | 350 000 | 245 000 | |

| May | 365 000 | 109 500 | |

| June | 120 000 |

RECEIPT-TREND FROM DEBTORS: (Must equal 100% of credit sales)

- Percentage of credit sales, over 2, 3 or 4 months.

- First portion (part) collected in the month of sale or in the month following the sales month:

- Is there a discount offered for receipts in the first month?

- Is provision made for bad debts?

EXAMPLE: The trend in the way debtors settle their accounts is as follows: 20% pay in the month of sale and receive a 5% discount.

35% pay in the month following the month of sale.

40% pay two months after the sales month.

The balance are bad debts.

4.2 Purchases and payments to creditors

At times, payment is made early to take advantage of a discount.

TOTAL PURCHASE AMOUNTS: (two possible options)

| 1. AMOUNTS ARE GIVEN | |||||||||||||||

| Purchase amounts are provided in the question. | |||||||||||||||

| Cash purchases are 20% of total purchases. | |||||||||||||||

Information:

| |||||||||||||||

| 2. COST OF SALES IS THE TOTAL AMOUNT PURCHASED | |||||||||||||||

| The business maintains a base stock and stock is replaced monthly. | |||||||||||||||

| Cash purchases are 20% of total purchases. The business uses a profit mark-up of 50% on cost. | |||||||||||||||

Information:

|

DO THE CALCULATIONS:

- The business maintains a base stock. Stock is replaced monthly.

- Calculate the cash and credit purchases for the three months.

- Identify the amount that will be paid in May 2017.

- Total sales:

2017 March April May R320 000 R350 000 R365 000 - Profit mark-up is 60% on cost.

- 20% of purchases are paid for in cash.

- Creditors are paid two months after the month of purchase.

| TOTAL SALES | COST OF SALES 100% | CASH PURCHASES 20% | CREDIT PURCHASES 80% | |

| MARCH | 320 000 | |||

| APRIL | 350 000 | |||

| MAY | 365 000 | |||

| Amount to be paid in May 2017: | ||||

LET’S PRACTICE: (Sales and Purchases)

The following information appeared in the books of Mouse Traders:

REQUIRED:

1.1 Complete the Debtors’ Collection Schedule for June and July 2018.

1.2 Complete the section of the Cash Budget to show cash sales, cash from debtors, cash

purchases and payments to creditors.

INFORMATION:

- The business uses a profit mark-up of 75% on cost.

- Sales:

- Cash Sales account for 20% of total sales.

- Debtors pay according to the following pattern:

- 30% in the month of sales, subject to a 5% discount.

- 50% in the month following the sales month.

- 18% two months after the sales month.

- Purchases:

- The business maintains a base stock. Stock is replaced in the same month that sales take place.

- Credit purchases makes up 60% of total purchases.

- Creditors are paid two months after the month of purchase.

- Schedule of total sales:

MARCH APRIL MAY JUNE JULY R61 250 R73 500 R64 750 R78 750 R70 000

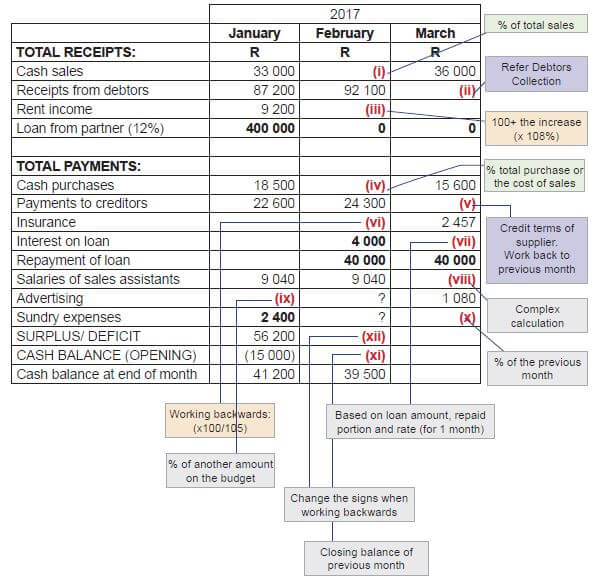

4.3 UNPACKING THE BUDGET: Examples of different calculations

ADDITIONAL INFORMATION:

- Cash sales is 30% of total sales.

February total sales is R130 000.

130 000 x 30%

39 000 - The amount must come from a Debtors Collection Schedule that must be prepared.

- Rent income increases by 8% from 9 200 x 108%

1 February 2017. 9 200 x 8% = 736; 9 200 + 736

9 936 - Cash purchases accounts for 20% of total purchases. Total purchases for February 2017 is R81 000.

81 000 x 20%

16 200 - Credit purchases are paid in 60 days (two months after purchase).

18 500 x 80/20

74 000 - Insurance will increase by 5% in March. 2 457 x 100/105

2 340 - The loan was received on 31 January 2017. A fixed instalment and interest are paid on the last day of each month.

Interest is not capitalized.

360 000

(400 000 - 40 000) x 12% x 1/12

3 600 - The business has four sales assistants; each earns the same wage. One sales assistant will receive a special bonus of 60% of her salary in March.

9 040/4 = 2 260 x 60%

9 040 + 1 356

(3 x 2 260) + (2 260 + 1 356)

10 396 - Advertising is estimated at a fixed percentage of monthly cash sales.

1 080/36 000 x 100 = 3%;

33 000 x 3%

990 - Sundry expenses increase by 5% each month.

2 400 x 105% = 2 520 x 105%

2 646 - Closing balance for the previous month is the opening balance for the next month.

41 200 - Surplus/ Deficit + Opening balance = Closing Balance

y + 41 200 = 39 500 y = 39 500 - 41 200

(1 700)

LET’S PRACTICE: (Calculations)

The following information appeared in the records of Abram Traders.

REQUIRED:

2.1 Complete the Debtors Collection Schedule.

2.2 Calculate the missing amounts in the budget for May and June.

2.3 Calculate the amount of the Fixed Deposit invested on 1 June.

INFORMATION:

A. Information for the budget period March - June 2018.

| ACTUAL | BUDGETED | |||

| MARCH | APRIL | MAY | JUNE | |

| Sales (cash and credit) | 148 500 | 168 000 | 142 500 | ? |

| Purchase of stock | 99 000 | 112 000 | ? | 103 000 |

| Rent Income | 11 200 | 11 200 | ? | ? |

| Manager’s Salary | 15 400 | 15 400 | ? | ? |

| Wages (Sales Assistants) | 19 500 | 19 500 | ? | ? |

| Advertising | ? | ? | ? | 2 438 |

| Commission expense | 4 455 | 5 040 | 4 275 | ? |

| Drawings | ? | ? | ? | ? |

| Interest on loan | 3 600 | 3 600 | ? | ? |

| Interest on fixed deposit | 0 | 0 | 0 | 540 |

| Sundry expenses | 8 000 | ? | ? | ? |

B. Additional Information:

- 25% of total sales are cash sales.

- Debtors pay according to the following trend:

60% pay in the month following the transaction month.

37% pay in the 2nd month after the transaction month.

03% written off as bad debt. - Stock is replaced in the month it was sold. A base stock is maintained.

- Goods are sold at a mark-up of 50% on cost.

- All purchases are made on credit. Creditors are paid in the following month and receive a 4% discount.

- Salaries and wages:

- The manager will receive a 10% increase on 1 June.

- The business employs three sales assistants on the same wage. They will receive a 6% inflationary increase on 1 May. One sales assistant will receive a bonus of 50% of her wages in June.

- Sundry expenses increase by 5% on the previous month.

- Rent income will increase by 9% on 1 May.

- Interest on loan is not capitalized. It is paid at the end of each month at 12% p.a. R50 000 of the loan will be paid on 31 May.

- The owner will draw R5 500 per month. R1 200 will comprise stock.

- The sales staff receive a commission equal to a fixed percentage of total sales.

- The advertising budget will increase by 6% on 1 June.

- A fixed deposit was invested on 1 June. Interest of 9% p.a. is receivable on 30 June.

ACTIVITY 1:

The information provided below relates to Brakpan Stationers.

REQUIRED:

1.1 Explain the importance of comparing budgeted figures with actual figures achieved for the same period. (2)

1.2 Calculate the missing amounts (indicated by a, b and c) in the Debtors’ Collection Schedule for the budgeted period March to May 2015. (4)

1.3 Calculate the following budgeted figures:

1.3.1 Total sales for March 2015. (2)

1.3.2 Payments to creditors during May 2015. (4)

1.3.3 Salaries of the shop assistants for April 2015. (3)

1.3.4 The % increase in the salary of the manager expected in May 2015. (3)

1.3.5 Amount of the additional loan expected to be acquired on 1 April 2015. (3)

1.4 An official of the local municipality has offered to recommend Brakpan Stationers supply the municipality with stationery to the value of R500 000.

However, he will only do this if he receives a cash payment of R20 000 from the owner.

What advice would you offer? State TWO points. (4)

1.5 The owner’s wife is angry that he has not been adhering to the cash budget. The owner says that he deliberately did not keep to the budget because he wanted to improve the overall results of the business.

- Identify THREE over-payments in April. Provide the figures to support your answer.

Provide a valid reason for each over-payment to support the owner’s decisions. (6) - Explain how the difference of opinion with his wife can be avoided in future. (2)

- State TWO other strategies that the owner and his wife could consider in future to improve the results of the business. (2)

INFORMATION

- Sales and debtors’ collection:

- TOTAL sales for April 2015 and May 2015 have been estimated as follows:

April 2015 70 000 May 2015 78 750 - 80% of all sales are cash sales. The rest of the sales are on credit.

- Debtors are expected to pay as follows:

- 60% within the month of sale, subject to a 4% discount.

- 38% in the month following the month of sale.

- 2% of debts are written off in the second month following the month of sale.

- Debtors’ collection schedule:

CREDIT SALES R MARCH R APRIL R MAY R February 31 500 11 970 March 10 500 a 3 990 April 14 000 8 064 b May c 18 018 12 054

- TOTAL sales for April 2015 and May 2015 have been estimated as follows:

- Purchase of merchandise and payments to creditors:

- A fixed-stock base is kept, i.e. the stock sold is replaced at the end of that month.

- The business uses a mark-up of 75% on cost.

- 70% of all merchandise is purchased on credit.

- Creditors are paid in full in the month following the month of purchase.

- Salaries:

Shop assistants- The business has 12 shop assistants who are employed on equal pay in March 2015.

Nine of the shop assistants are entitled to a bonus equal to 80% of the monthly salary in April 2015. - All shop assistants will receive a general increase in May 2015.

- The business has 12 shop assistants who are employed on equal pay in March 2015.

- Loan:

An additional loan will be taken from Atlantic Bank on 1 April 2015. The interest rate is 14% p.a. - Extract from the Cash Budget for the three months ending 31 May 2015:

| RECEIPTS | MARCH | APRIL | MAY | |

| Budgeted | Budgeted | Actual | Budgeted | |

| Cash sale of stock | 42 000 | 56 000 | 59 200 | 63 000 |

| Collections from debtors | 18 018 | 12 054 | 12 800 | ? |

| Rent income | 5 600 | 6 160 | 6 160 | 6 160 |

| Additional loan acquired | 0 | ? | ? | 0 |

| PAYMENTS | ||||

| Cash purchase of stock | 9 000 | 12 000 | 28 000 | 13 500 |

| Payment to creditors | 58 500 | 21 000 | 21 000 | ? |

| Salaries of shop assistants | 102 000 | ? | ? | 110 160 |

| Salary of manager | 16 000 | 16 000 | 40 000 | 19 200 |

| Interest on loan (14% p.a.) | 6 300 | 7 175 | 7 175 | 7 175 |

| Delivery expenses to customers | 9 200 | 9 200 | 0 | 9 200 |

| Insurance (paid annually) | 0 | 27 000 | 27 000 | - |

| Advertising | 0 | 0 | 0 | 20 000 |

| Purchase of vehicle | 0 | 0 | 180 000 | 0 |

| Vehicle expenses | 0 | 0 | 4 000 | 4 000 |

| Sundry expenses | 5 300 | 5 300 | 5 300 | 5 800 |

ACTIVITY 2:

You are provided with a partially completed Projected Income Statement for Dawn Distributors for the period 1 October 2015 to 31 December 2015. It was prepared by the bookkeeper.

REQUIRED:

2.1 List TWO items on the Projected Income Statement,that would not appear on a Cash Budget. (2)

2.2 Fill in the missing amounts denoted by A to E on the Projected Income Statement. (16)

2.3 Take the following additional information into account and calculate the following:

2.3.1 The percentage increase in the wages of cleaners in December 2015. (4)

2.3.2 The monthly salary due to the sales manager in December 2015. (4)

2.3.3 Total credit sales expected in December 2015. (3)

2.3.4 The balance of the loan on 1 November 2015. (3)

INFORMATION:

- The business uses a mark-up percentage of 60% on cost.

- Credit sales comprise 75% of total sales.

Sales are expected to increase by 10% per month and by 20% during December. - The business employs a sales manager and an administration manager. The sales manager earns R300 more than the administration manager (per month). The managers are entitled to an increase of 8% p.a. from 1 December 2015.

- R20 000 of the loan is repayable on 30 November 2015. Interest on loan at 9% p.a. is payable every quarter. The next payment is due on 1 January 2016.

- Advertising expense per month is budgeted at a fixed percentage of total sales.

- Income tax is estimated to be 30% of the net profit before tax.

G. INFORMATION FROM THE PROJECTED INCOME STATEMENT FOR OCTOBER TO DECEMBER 2015.

OCTOBER | NOVEMBER | DECEMBER | ||

BUDGETED | ACTUAL | BUDGETED | BUDGETED | |

Sales | 120 000 | 98 400 | 132 000 | ? |

Cost of sales | 75 000 | 58 800 | B | 99 000 |

Gross profit | A | ? | ? | |

Other income | 20 700 | 18 200 | 20 700 | 21 200 |

Rent income | 10 000 | 10 000 | 10 000 | 10 000 |

Discount received | 1 200 | 1 000 | 1 200 | 1 200 |

Commission income | 9 500 | 7 200 | 9 500 | 10 000 |

Gross operating income | ||||

Operating expenses | 48 300 | ? | ? | |

Salaries (managers) | 17 100 | 17 100 | 17 100 | D |

Wages (cleaners) | 3 200 | 3 200 | 3 200 | 3 376 |

Maintenance | 4 000 | 1 650 | 4 000 | 4 000 |

Telephone | 2 000 | 4 280 | 2 000 | 2 500 |

Insurance | 1 800 | 1 800 | 1 800 | 1 800 |

Advertising | 2 400 | 1 900 | C | 3 168 |

Depreciation | 6 200 | 8 000 | 6 200 | 8 000 |

Trading stock deficit | 0 | 680 | 0 | 500 |

Stationery | 3 150 | 3 100 | 3 200 | 3 250 |

Sundry operating expenses | 8 450 | 8 420 | 8 500 | 8 550 |

Operating profit | 17 400 | ? | ? | |

Interest income | 225 | 200 | 200 | 200 |

Profit before interest expense | 17 625 | |||

Interest expense | 585 | 585 | 585 | 435 |

Net profit before income tax | ? | ? | ? | |

Income tax | ? | ? | ? | |

Net profit after tax | E | ? | ? | |

4.4 ANALYSING AND INTERPRETING BUDGET INFORMATION

Frequently asked Questions (FAQ)

- Comparing ACTUAL AMOUNTS to BUDGETED AMOUNTS.

The difference is referred to as a VARIANCE.ACTUAL AMOUNT

EXPLANATION

Well controlled

The actual amount is equal to or very close to the budgeted amount.

Over-budget

Under-spending. The amount is significantly lower than the budgeted amount.

Under-budget

Over-spending. The amount is significantly higher than the budgeted amount.

- Possible reason for the difference (variance).

- Possible solutions/ advice/ recommendations (internal controls).

ACTUAL AMOUNT

POSSIBLE REASON

SOLUTION/ADVICE

Well controlled

Well managed and communicated.

Over-budget

Incorrect budgeting; trying to cut costs; lack of supervision; negligence. unrealistic budgeting.

Adjust the budget; do not attempt to cut the cost of essential services; always consult the budget.

Under-budget

Lack of supervision; no company rules; abusing privileges, unrealistic budgeting.

Investigate; set rules; supervise; adjust the budget if necessary.

RELATE THE REASON/ ADVICE TO THE SPECIFIC ITEM BEING ANALYSED.

EXAMPLE:

Kobus is concerned about the following items, which were under/ over budget for February 2016:

Item | Budgeted | Actual | Under/ over budget |

Collections from debtors | 174 200 | 61 800 | Under |

Payments to creditors | 39 400 | 15 600 | Under |

Insurance | 2 260 | 0 | Under |

Drawings | 18 000 | 52 000 | Over |

Explain why each of the items reflects a problem for the business and advise Kobus regarding each case.

Item | Explanation |

Collection from debtors | Any two valid reasons

|

Payments to creditors | Any two valid reasons

|

Insurance | Any two valid reasons

|

Drawings | Any two valid reasons

|

- OTHER INTERPRETIVE SCENARIOS:

- Related Receipts (income) and Payments (expenses)

- Sales is influenced and affected by Advertising, Delivery Expenses, Commission Expenses and Packing Material.

- Rent or buy decisions

- Property or fixed assets such as machinery. Take into consideration the availability of finance, the cost of borrowing, the long-term benefits of the asset etc.

- Identifying steps taken by the owner to correct/ improve the cash-flow situation:

- Observe the pattern of the cash balance (positive/ overdraft).

- Wasteful expenditure.

- Introduction of additional capital, loans or investments.

- Related Receipts (income) and Payments (expenses)

ACTIVITY 3:

Below is information relating to DIY Hardware. The business is owned by John Temba. His inexperienced bookkeeper, Mabel, has prepared a Cash Budget.

REQUIRED:

3.1 Identify TWO items that Mabel has incorrectly entered in the Cash Budget. (4)

3.2 Apart from the items mentioned above, name TWO other items in the Payments Section of the Cash Budget that would NOT appear in a Projected Income Statement. (4)

3.3 After correcting all the errors John has identified the following:

JAN 2013 | FEB 2013 | |

Cash deficit for the month | (14 950) | (52 400) |

Cash at the beginning of the month | 35 350 | |

Cash at the end of the month | A | B |

Identify or calculate A and B. Indicate negative figures in brackets. (3)

3.4 Identify or calculate the missing figures C and D in the extract from the Cash Budget. (7)

3.5 Complete the Debtors’ Collection Schedule for February 2013. (10)

3.6 Calculate the percentage increase in salary and wages from 1 February 2013. (2)

3.7 Calculate the interest on the fixed deposit for January 2013. (2)

3.8 John pays Speedy Deliveries to deliver hardware to his customers free of charge. He budgets for this at a rate of 8% of total monthly sales.

3.8.1 Calculate the delivery expense figure budgeted for January 2013. (2)

3.8.2 John is of the opinion that the delivery service is costing him too much.

Which TWO points should John consider before deciding on whether or not to discontinue this service? (4)

3.9 On 31 January 2013 you identified the figures below. Explain what you would say to John about each of the following items at the end of January 2013. Give ONE point of advice in each case. (9)

JANUARY 2013 | ||||

BUDGETED | ACTUAL | |||

Advertising | 1 600 | 0 | ||

Stationery | 1 000 | 4 400 | ||

Staff training | 2 000 | 700 | ||

3.10 John will have a problem with replacing his old computers and cash registers in March 2013. The cost of these items amounts to R150 000 and he expects them to last 5 years. However, he does not have cash available to pay for this. His options are:

- Raise a new loan at an interest rate of 14% p.a. to be repaid over 36 months.

- Hire (Lease) the assets from IT Connect Ltd at R5 100 per month.

- Invite his friend James to become an equal partner in the business and provide capital of R150 000.

John realizes that all three options have the advantage of not requiring the R150 000 outlay in March 2013.

Consider each of these options and explain ONE other advantage and ONE disadvantage of each option. Provide figures to support your answer. (6)

INFORMATION:

- Sales, purchase of stock and cost of sales:

- Total sales for November 2012 to February 2013 were as follows:

- November: R150 000

- December: R200 000

- January: R160 000

- February: R140 000

- 60% of all sales are cash sales; the rest is credit sales.

- The mark-up is 33.3% on cost of sales at all times.

- Stock is replaced on a monthly basis.

- 50% of all purchases are cash, the rest is on credit.

- Total sales for November 2012 to February 2013 were as follows:

- Debtors’ collection:

Debtors are expected to pay as follows:- 30% of debtors pay their accounts in the month of sale (current).

- 50% pay in the month following the sales transaction month (30 days).

- 8% pay in the second month (60 days).

- 2% are written off.

- Creditors’ payment:

Creditors are paid in the month after purchases, so as to receive a 5% discount. - EXTRACT FROM THE CASH BUDGET FOR JANUARY AND FEBRUARY 2013

JAN 2013

FEB 2013

RECEIPTS

Cash sales

96 000

84 000

Collection from debtors

70 000

?

Interest on fixed deposit (7% p.a.)

?

0

Fixed deposit: Magic Bank maturing on 1 Feb. 2013

0

42 000

Commission income

?

?

Rent income

8 500

8 800

PAYMENTS

Salary and wages

15 000

16 800

Stationery

1 000

1 000

Telephone

?

?

Payment to creditors

71 250

D

Cash purchase of stock

C

52 500

Repayment of existing loan

100 000

Furniture bought on credit

30 000

Delivery expense for delivery of hardware to customers

?

11 200

Training of staff

2 000

2 000

Advertising

1 600

1 400

Depreciation

12 500

12 500

Sundry expenses

3 500

3 600

Drawings by owner

?

?

Vehicle expenses

0

500

ACTIVITY 4: (40 marks; 25 minutes)

4.1 Explain why:

4.1.1 Depreciation and bad debts will not appear in a Cash Budget. (2)

4.1.2 A cash budget is different from a Projected Income Statement. (2)

4.2 KIT KAT DISTRIBUTORS LTD

You are provided with information for the budget period November and December 2018.

REQUIRED:

4.2.1 Complete the Debtors’ Collection Schedule. (12)

4.2.2 Calculate the missing amounts in the Cash Budget denoted by (i) to (iv). (20)

4.2.3 Comment on the internal controls on collection from debtors and payment to creditors. Provide TWO points. (4)

INFORMATION:

A. Cash sales amount to 40% of total sales.

Goods are marked-up by 25% on cost.

B. Debtors are granted credit terms of 30 days. The actual collection trend revealed that:

- 50% of debtors pay in the month of the sale to receive a 5% discount.

- 30% is received in the month following the month of sales.

- 18% is collected in the second month after the sale.

- 2% of debtors is written off.

C. Stock is replaced in the month it was sold, i.e. a base stock is maintained.

D. 80% of stock is bought on credit. Creditors are paid in full in the month following the month the purchase was made.

E. Salaries and wages are expected to remain the same for the budget period. Staff members on leave in December will receive their pay in November - the total amount is R35 600.

F. A loan will be received from a director, Thabo, on 1 November 2018, at 13% interest p.a. Interest is not capitalised. A fixed monthly instalment and interest will be paid at the end of each month.

G. The company will pay an interim dividend in December. H Rent increased by 8% on 1 November 2018.

I. Incomplete Debtors’ Collection Schedule:

MONTH | CREDIT SALES | NOVEMBER | DECEMBER |

September | 180 000 | 32 400* | |

October | 186 000 | 55 800 | * |

November | * | 92 625 | * |

December | 210 000 | * | |

TOTAL | * | * |

J. Information from the Projected Income Statement:

NOVEMBER 2018 | |

Sales | 325 000 |

Cost of sales | 260 000 |

Commission income | 24 800 |

Depreciation | 12 600 |

Interest expense | 1 625 |

K Incomplete Cash Budget for 2018:

RECEIPTS | NOVEMBER | DECEMBER |

Cash sales | 130 000 | (i) |

Cash from debtors | ||

Commission income | 24 800 | 26 000 |

Rent income | (ii) | 19 710 |

Loan from director Thabo | 150 000 | 0 |

TOTAL RECEIPTS | ||

PAYMENTS | ||

Cash purchases of stock | 52 000 | 56 000 |

Payments to creditors | (iii) | 208 000 |

Directors fees | 20 000 | 20 000 |

Salaries and wages | 180 600 | (iv) |

Loan instalment (including interest) | 13 625 | (v) |

Interim dividends | 0 | 86 500 |

Sundry expenses | 15 875 | 16 510 |

TOTAL PAYMENTS |

Start-up Activity

Place the correct amount in the respective column/s.

Note that amounts can go in more than one column.

| NO | INFORMATION | CASH BUDGET | PROJECTED INSOMCE STATEMENT | ||

| RECEIPT | PAYMENT | INCOME | EXPENSE | ||

| a | Cash sales are expected to be R7 400 per month at a 25% mark-up on cost. | 7 400 | 7 400 | 5 920 | |

| b | An old computer with a carrying value of R4 400 will be sold for R2 500 cash in the next month. | 2 500 | 1 900 | ||

| c | Depreciation on equipment is estimated to be R950 per month. | 950 | |||

| d | An annual insurance premium of R5 200 is paid by cheque. R1 200 is for the next financial year. | 5 200 | 4 000 | ||

EXAMPLE: Cash sales amounts to 30% of total sales.

Calculate the missing amounts.

TOTAL SALES 100% | CASH SALES 30% | CREDIT SALES 70% | |

March | 320 000 | 96 000 | 224 000 |

April | 350 000 | 105 000 | 245 000 |

May | 365 000 | 109 500 | 255 500 |

June | 400 000 | 120 000 | 280 000 |

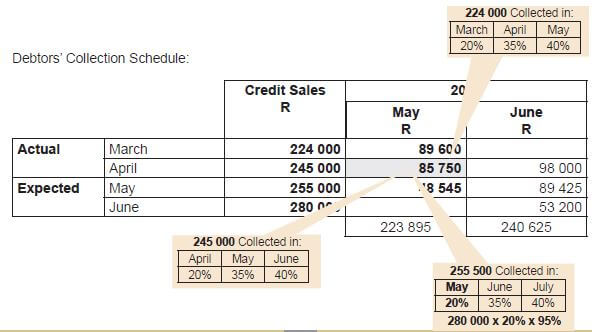

Debtors’ Collection Schedule:

| Credit Sales R | 2017 | |||

| May R | June R | |||

| Actual | March | 224 000 | 89 600 | |

| April | 245 000 | 85 750 | 98 000 | |

| Expected | May | 255 000 | 48 545 | 89 425 |

| June | 280 000 | 53 200 | ||

| 223 895 | 240 625 | |||

DO THE CALCULATIONS: PURCHASES AND PAYMENTS TO CREDITORS

TOTAL SALES | COST OF SALES 100% | CASH PURCHASES 20% | CREDIT PURCHASES 80% | |

MARCH | 320 000 | 320 000 x 100/160 | 40 000 | 160 000 |

APRIL | 350 000 | 350 000 x 100/160 | 43 750 | 175 000 |

MAY | 365 000 | 365 000 x 100/160 | 45 625 | 182 500 |

| Amount to be paid in May 2017 | 160 000 | |||

1.1 LET’S PRACTICE: (Sales and Purchases)

MONTH | CREDIT SALES | MAY | JUNE | JULY |

March | 49 000 | 8 820 | ||

April | 58 800 | 29 400 | 10 584 | |

May | 51 800 | 14 763 | 25 900 | 9 324 |

June | 63 000 | 17 955 | 31 500 | |

July | 56 000 | 15 960 | ||

| CASH FROM DEBTORS | 52 983 | 54 439 | 56 784 | |

1.2 CASH BUDGET (EXTRACT)

CASH RECEIPTS | MAY | JUNE | JULY |

Cash sales | 12 950 | 15 750 | 14 000 |

Cash from debtors | 52 983 | 54 439 | 56 784 |

CASH PAYMENTS | |||

Cash purchases of stock | 14 800 | 18 000 | 16 000 |

Payments to creditors | 21 000 | 25 200 | 22 200 |

Workings: Calculation of the cost of sales and credit purchases:

MARCH | APRIL | MAY | JUNE | JULY | |

Sales | R61 250 | R73 500 | R64 750 | R78 750 | R70 000 |

Cost of Salesx 100/175 | 35 000 | 42 000 | 37 000 | 45 000 | 40 000 |

Credit Purchases COS x 60% | 21 000 | 25 200 | 22 200 | 27 000 | 24 000 |

LET’S PRACTICE (Calculations)

2.1 DEBTORS COLLECTION SCHEDULE

MONTHS | CREDIT SALES | MAY | JUNE | |

March | 111 375 | 52 725 | ||

April | 126 000 | 75 600 | 46 620 | |

May | 106 875 | 64 125 | ||

June | ||||

128 325 | 111 745 |

2.2 CASH BUDGET FOR THE PERIOD 1 MAY - 30 JUNE

MAY | JUNE | |

Cash sales | 35 625 | 38 625 |

Cash from debtors | 128 325 | 111 745 |

Rent income | 12 208 | 12 208 |

Payments to creditors | 107 520 | 91 200 |

Manager’s salary | 15 400 | 16 940 |

Wages (shop assistants) | 20 670 | 24 115 |

Interest on loan | 3 600 | 3 100 |

Commission expense | 4 275 | 4 635 |

Sundry expenses | 8 820 | 9 261 |

Advertising | 2 300 | 2 438 |

Drawings | 4 300 | 4 300 |

2.3 Calculate the amount of the Fixed Deposit invested on 1 June.

- 540 x 12 = 72 000

9%

ACTIVITY 1: BRAKPAN STATIONERS

1.1 Explain the importance of comparing budgeted figures with actual figures achieved for the same period.

One valid explanation

- Deviations can be determined and remedial measures can be put in place.

- Establish whether the budgeting was realistic.

- To identify trends of mismanagement of cash. (2)

1.2 Calculate the missing amounts (indicated by a, b and c) in the Debtors’ Collection Schedule for the budgeted period March to May 2015 (4)

| a | 6 048 |

| b | 5 320 |

| c | 15 750 |

1.3.1 Calculate budgeted total sales for March 2015. (2)

- 10 500 x 100/20 = 52 500

1.3.2 Calculate the amount budgeted for payments to creditors during May 2015. (4)

- 40 000

70 000 x 100/175 x 70% = 28 000 any one part correct

or

12 000/30 x 70 = 28 000

1.3.3 Calculate the budgeted salaries of the shop assistants for April 2015. (3)

- 102 000/12 = 8 500 8 500 x 3 = 25 500

15 300 x 9 = 137 700

25 500 + 137 700 = 163 200 any one part correct

OR: 102 000 one mark + 61 200 one mark = 163 200

(102 000 X 80% X 9/12)

1.3.4 Calculate the % increase in the salary of the manager expected in May 2015. (3)

- 3 200 (1 mark)

(19 200 - 16 000) /16 000 = 20% any one part correct

1.3.5 Calculate the amount of the additional loan expected to be acquired on 1 April 2015. (3)

- 875 x (100 x12) /14 = 75 000 any one part correct

1.4 An official of the local municipality has offered to recommend that Brakpan Stationers supply the municipality with stationery to the value of R500 000. However, he will only do this if he is paid R20 000 in cash.

Give advice in this regard. State TWO points.

Any two suggestions (4)

- This is actually a bribe, which is unethical.

- If this information is made public, it will have a negative effect on the business.

- The owner must submit a formal tender to secure a contract through the normal processes.

1.5 Identify THREE over-payments made in April. Provide figures to support your answer. Provide a valid reason for each over-payment to support the decision taken. (6)

| Over-payment with figures Item and figure | Valid reason | |

| 1 | The bonus paid to the manager in February 2015 (R24 000) was not taken into account. | He has retained the services of a valuable employee. |

| 2 | Purchase of vehicle (R180 000). | The difference between motor vehicle expenses and delivery expenses is R5 200 per month. |

| 3 | Cash purchase of merchandise (R28 000) was significantly higher than the budgeted figure (R12 000). | Possibly to take advantage of discounts on bulk purchases. |

1.6 Explain how this difference of opinion with his wife can be avoided in future.

- They should have a specific meeting to determine the budget jointly and the owner should consult his wife before spending on unbudgeted items.

State TWO other strategies that the owner and his wife could consider in future to improve the results of the business.

Any two valid points:

- Advertise monthly. / Reduce the number of shop assistants.

- Reinstate deliveries to customers. / Negotiate longer credit terms with suppliers.

ACTIVITY 2 : DAWN DISTRIBUTORS

2.1 Identify TWO items that Mabel has incorrectly entered in the Cash Budget.

Any TWO

- Cost of sales / Discount received / Depreciation / Trading stock deficit

2.2

| A | Gross profit | 120 000 - 75 000 = 45 000 |

| B | Cost of sales | 132 000 x 100/160 = 82 500 Or 132 000 x 62,5% or 132 000 - (132 000 x 37,5%) |

| C | Advertising | 2 400/120 000 = 2% 132 000 x 2% = 2 640 |

| D | Salaries | 17 100 x 108% = 18 468 Or 17 100 + 1 368 = 18 468 |

| E | Net Profit after tax | 17 040 (17 625 - 585) x 30% = 5 112 17 040 - 5 112 = 11 928 |

2.3.1 The percentage increase in wages that the cleaners will receive in December 2015.

- 176

(3 376 - 3 200) x 100 = 5,5% (one part correct)

3 200

2.3.2 The monthly salary due to the Sales Manager in December 2015.

- (17 100 - 300) = 8 400 (8 400 + 300) x 108% = 9 396 (one part correct)

2

2.3.3 Total credit sales expected in December 2015.

- (99 000 x 160% ) x 75% = 118 800 (one part correct)

OR

132 000 X 120% = 158 400 X 75% = 118 800

2.3.4 The balance of the loan on 1 November 2015.

- 585 x 1200/9 = 78 000 (one part correct)

ACTIVITY 3: DIY HARDWARE

3.1 Identify TWO items that Mabel has incorrectly entered in the Cash Budget.

Two items

- Depreciation

- Furniture bought on credit

3.2 Apart from the items above, name TWO other items in the Payments Section of the Cash Budget that would NOT appear in a Projected Income Statement.

Any two items

Expected responses:

- Payment to creditors / Repayment of loan / Purchase of vehicle / Drawings Cash purchases of stock

3.3 Identify or calculate A and B. Indicate negative figures in brackets.

| A | R35 350 |

| B | (R17 050) |

3.4 Identify or calculate the missing figures C and D in the extract from the Cash Budget

C | 160 000 x 100/133⅓ = 120 000; 120 000 x 50% = R60 000 | ||

D | 60 000 x 95% = 57 000 any one part correct |

3.5 Complete the Debtors’ Collection Schedule for February 2013.

Credit sales | February collections | |

December | R80 000 | 14 400 |

January | R64 000 | 32 000 |

February | R56 000 | 16 800 |

| TOTAL operation | 63 200 | |

3.6 Calculate the % increase in salary and wages with effect from 1 February 2013.

- 1 800 /15 000 x 100 = 12 %

3.7 Calculate interest on the fixed deposit for January 2013.

- 42 000 x 7% / 12 = R245

3.8.1 Calculate delivery expenses for January 2013.

- R160 000 x 8% = R12 800

3.8.2 John is of the opinion that the delivery service is costing him too much. Which TWO points should John consider before deciding whether or not to discontinue this service?

Two factors

- Whether his competitors are offering the service or not.

- What the reaction from his customers will be should he withdraw the service.

- The possibility of charging customers for the delivery service.

- The possibility of finding a cheaper delivery service.

- The possibility of using his own vehicle instead of sub-contracting this service.

3.9 Explain what you would say to John about each item at the end of January 2013. Give ONE point of advice in each case.

| Comment | Advice | |

| Advertising | As he did not spend any money on Advertising, this will probably mean that he will not achieve budgeted sales. | Make sure that he utilises the advertising budget fully each month. (It is there for a purpose.) |

| Stationery | He spent significantly more than the budgeted figure. | Ensure that there is no wastage of stationery. / Keep unused stationery secured. / Find a cheaper supplier. |

| Staff training | He under-spent on the budget, which means that staff might not be interacting well with customers. | He must consider that staff training affects the manner in which staff interact with customers. This leads to efficiency and goodwill. |

3.10 Consider each of the options below and explain ONE other advantage and ONE disadvantage related to each option.

| Other Advantage | Diadvantage | |

| Option 1: Raise a new loan to be repaid over 36 months. The interest rate is 14% p.a.. | He will own the assets and they could last longer than five years if he takes good care of them. | He has to pay interest of R1 750 per month + R4 167 per month to repay the loan. |

| Option 2: Hire (lease) the assets from IT Connect Ltd at R5 100 per month. | He does not have to raise a loan. / He does not have to pay interest on the loan./ He will not have to pay repair costs. | The lease charges are expensive, at R5 100 per month (R306 000 over the expected life span of five years.) / He never owns the assets and so continues to pay. |

| Option 3: Invite his friend James to become an equal partner in the business and to provide capital of R150 000. | He will have the necessary funds to purchase the assets which will then belong to, the business / They will share the workload and their skills. | He will have to share half his profits with his new partner. |

ACTIVITY 4 :

4.1 Explain why:

4.1.1 Depreciation and bad debts will not appear in a Cash Budget.

Any valid explanation.

- Non-cash items are not included in a cash budget.

- A cash budget only includes cash receipts and cash payments.

4.1.2 A cash budget is different from a Projected Income Statement.

Any valid explanation.

- A cash budget includes receipts and payments and shows plans for cash management. It shows the surplus/ deficit and the bank balance.

- The PIS shows income and expenses (including non-cash items) and projects the profit or loss per month (for the budget period).

4.2 KIT KAT DISTRIBUTORS LTD

4.2.1

MONTHS | CREDIT SALES | NOVEMBER | DECEMBER |

September | 180 000 | 32 400 | |

October | 186 000 | 55 800 | 33 480 |

November | 195 000 | 92 625 | 58 500 |

December | 210 000 | 99 750 | |

| Total collection from debtors | 180 825 | 191 730 | |

4.2.2 Calculate:

- Cash sales for December:

210 000 X 40/60 = 140 000 - Rent income amount for November:

19 710 x 100/108 = 18 250 - Payments to creditors for November:

186 000 x 100/60 = 310 000

310 000 x 100/125 = 248 000

248 000 x 80%

= 198 400 - Salaries and wages for December:

180 600 - 35 600 - 35 600

= 109 400 - Loan instalment (including interest) for December:

138 000

(13 625 - 1 625) + (150 000 - 12 000) x 13% x 1/12

12 000 1 495 (three marks)

= 13 495

4.2.3 Comment on the internal controls for collection from debtors and payments to creditors. Provide TWO points.

Any TWO valid points.

- Only 50% of the debtors comply with the credit terms.

- The cash from debtors does not cover the payments to creditors every month.

- 80% of stock is bought on credit. / Only 20% is cash purchase of stock.

- As cash sales is a greater percentage of total sales, it may be wise to increase the percentage of cash purchases.

- Taking advantage of short-term credit is only beneficial if it eases cash-flow problems.

6. Message to grade 12 learners from the writers

“Begin with the end in mind.”

Stephen Covey

At the end of your journey in the GET phase, you were required to choose a subject set that will shape your career path. Hopefully, your choice was based on your aptitude, ambition and desire

to become a successful individual, with a comfortable standard of living.

Let’s be frank! Accounting is not for the faint-hearted. There are NO short-cuts. Success in

Accounting demands hard work and dedication, but the rewards are satisfying.

The questions and topics covered in the examination papers are very predictable. You need

to just extract the NSC papers for the last three years from the internet and compare the questions. If you do this, you will become familiar with the commonly sked questions and the style and format of the paper. You will also gain insight into the different ways in which questions

can be asked.

Practice every day, do not be afraid to ask questions, engage in group studies and attend the

many intervention programmes organized by your school and your Department of Education.

Effective planning will ensure that you:

Know the rules of the game and play it better than others.

7. Thank you

This Accounting module on the Analysis and Interpretation of financial information was developed by Mr P Govender, Mr A Leeuw, Mr M.P Shabalala, Mr Dorian Olifant and Ms ZJM Mampana (Subject Specialists, PED)

A special mention must be made of Mr Mzikaise Masango, the DBE curriculum specialist who, in addition to his contribution to the development of the guide, also coordinated and finalised the process.

These officials contributed their knowledge, experience and in some instances unpublished which they have gathered over the years to the development of this resource. The Department of Basic Education (DBE) gratefully acknowledges these officials for giving up their valuable time, families and expertise to develop this resource for the children of our country.

Administrative and logistical support was provided by Mr Noko Malope and Ms Vhuhwavho Magelegeda. These officials were instrumental in the smooth and efficient management of the logistical processes involved in this project.

Look out for more modules that deal with other topics of the Grade 12 syllabus.