ACCOUNTING Past Paper FEBRUARY/MARCH 2016 Memorandum / Memo - GRADE 12 NATIONAL SENIOR CERTIFICATE

Share via Whatsapp Join our WhatsApp Group Join our Telegram GroupNATIONAL SENIOR CERTIFICATE - GRADE 12

ACCOUNTING

FEBRUARY/MARCH 2016

MEMORANDUM

MARKS: 300

MARKING PRINCIPLES:

- Penalties for foreign items are applied only if the candidate is not losing marks elsewhere in the question for that item (no foreign item penalty for misplaced item). No double penalty applied.

- Full marks for correct answer. If the answer is incorrect, mark the workings provided.

- If a pre-adjustment figure is shown as a final figure, allocate the part-mark for the working for that figure (not the method mark for the answer).

- Unless otherwise indicated, the positive or negative effect of any figure must be considered to award the mark. If no + or – sign or bracket is provided, assume that the figure is positive.

- Where indicated, part-marks may be awarded to differentiate between differing qualities of answers from candidates.

- This memorandum is not for public distribution, as certain items might imply incorrect treatment. The adjustments made are due to nuances in certain questions

- Where penalties are applied, the marks for that section of the question cannot be a final negative.

- Where method marks are awarded for operation, the marker must inspect the reasonableness of the answer before awarding the mark.

- In awarding method marks, ensure that candidates do not get full marks for any item that is incorrect at least in part.

- Codes: f = foreign item; p = placement/presentation.

Question 1

1.1 Explain how the Creditors' Reconciliation Statement can assist the business in terms of their internal control measures. State TWO points.

TWO valid points √√ √√

• It will assist the business in detecting errors/omissions in their books.

• It will show errors/omissions in the statement received.

• Detect fraudulent activities and take action

1.2 Calculate the correct balance of Pikor Suppliers in the Creditors' Ledger Account of Machu Traders. Show the changes to the figure R116 400.

(5 400 x 2)

116 400√+ 780√ - 480√√- 27 300√√ - 810√√- 10 800√√

= 77 790√√one part correct

1.3 Creditors' Reconciliation Statement for Pikor Suppliers on 30 April 2015.

| Details | Amount | |

| Balance per statement of account | 121 800 | √ |

| Credit amount to correct invoice over stated | (30 000) | √√ |

| Debit amount wrongly credited | 84 000 | √√ |

| Transfer of balance | (3 600) | √√ |

| Credit payment after statement date | (93 000) | √ |

| Credit discount after statement date | (1 410) | √ |

| Correct balance one part correct | 77 790 | √ |

1.4 The owner of Machu Traders is not completely satisfied with the service and quality of goods received from Pikor Suppliers. Suggest TWO factors he should consider before changing suppliers.

TWO valid factors √√ √√

- The credit terms offered

- Will they offer discount for early payments

- Will alternative supplier be able to meet the demands of the business

- The quality of the products they are able to deliver

Question 2

2.1.1 False √

2.1.2 False √

2.1.3 True √

2.2 STAR WHEELS MANUFACTURERS

2.2.1 DIRECT LABOUR COST

| Basic salary (14 x 7 000) √ x 12 √ 98 000 one part correct | 1 176 000 | √ |

| Overtime (14 x 144) √ x 65 √ | 131 040 | √ |

| UIF contributions (1 176 000 x 1%) (1% of basic) | 11 760 | √√ |

| one part correct | 1 318 800 | √ |

FACTORY OVERHEAD COST

| Indirect materials one part correct (13 200√ + 38 400 √ – 15 100 √) | 36 500 | √ |

| Salaries: foreman | 156 000 | √√ |

| Electricity and water (104 000 x 90%) | 93 600 | √√ |

| Rent expense (115 200 x 600/1 500) | 46 080 | √√ |

| Insurance (74 200 x 3/7) | 31 800 | √√ |

| Depreciation: factory plant and machinery | 277 220 | √ |

| operation | 641 200 | √ |

2.2.2 PRODUCTION COST STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2015.

| Direct (raw) materials cost | 2 100 000 | |

| Direct labour cost see 2.2.1 | 1 318 800 | √ |

| Prime cost operation | 3 418 800 | √ |

| Factory overhead costs see 2.2.1 | 641 200 | √ |

| Total manufacturing cost operation | 4 060 000 | √ |

| Work-in-process (beginning of year) | 160 000 | |

| operation | 4 220 000 | √ |

| Work-in-process at end operation | (220 000) | √ |

| Cost of production of finished goods (4 015 000 √ + 95 000 √ – 110 000 √) | 4 000 000 one part correct | √ |

2.3

2.3.1 Calculate the break-even point for the year ended 31 October 2015.

736 000/(28√-16√) = 61 333 or 61 334 units √ one part correct

2.3.2 Should the business be satisfied with the number of units that they have produced and sold during the current financial year? Explain. Quote figures.

Yes/No √

Reason with figures √√

Reasons for Yes

The business sold (64 000 – 61 334) 2 666 units more than the break-even point.

Reasons for No

The business sold (78 000 – 60 000) 18 000 more than the break-even point in the previous financial year.

Production decreased from 78 000 – 64 000

2.3.3 Give TWO possible reasons for the increase in the direct material cost per unit in the current financial year.

Any two suitable reasons √√ √√

- Due to the effects of inflation, price of raw materials increased.

- Storage costs.

- Raw material obtained from new suppliers.

- Increase in wastage

- Increase in carriage

2.3.4 Craig suggests that, in order to improve financial results in the new financial year, the quantity of cereal per box must be reduced by 10% and the selling price must remain the same. Give TWO valid reasons why he should not do this.

Any TWO valid reasons √√ √√

- It is not ethical and would lead to a decrease in the customers once this information becomes public knowledge.

- This is deliberate product shrinkage to gain higher profits. Could lead to legal action against the business.

- Product may be removed from the shelves if the contents of the product do not correspond with the information on the package.

Question 3

3.1 VAT CONCEPTS

| 3.1.1 | Output VAT √ |

| 3.1.2 | South African Revenue Services (SARS) √ |

| 3.1.3 | 0% (Zero) √ |

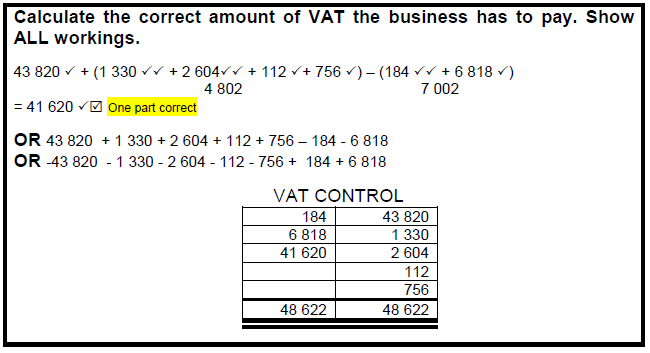

3.2 VAT CALCULATIONS

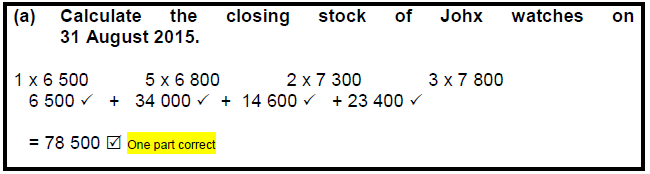

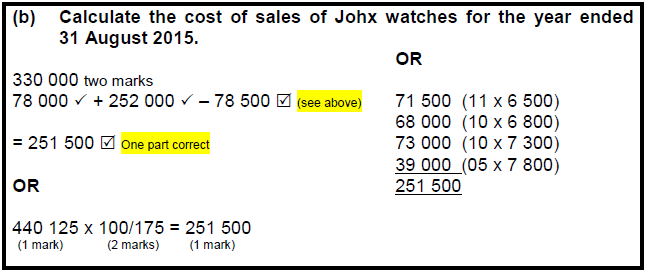

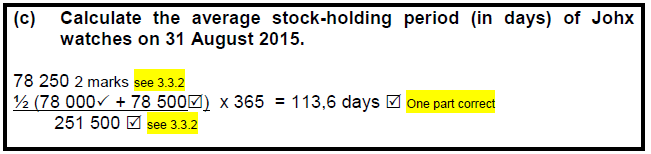

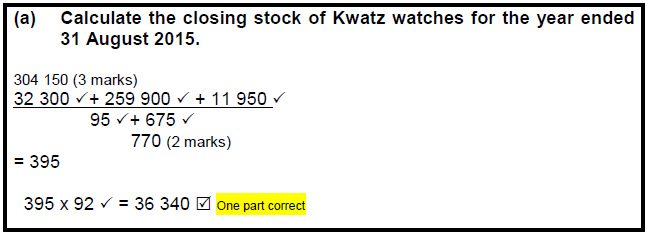

3.3 INVENTORY VALUATION

3.3.1

3.3.2

3.3.3 Explain why the business uses different methods to value each type of watch. State ONE valid point.

One valid point √√

- Johx is sold at a high value. Small quantities are purchased.

- Each item can be monitored individually.

- The value is continuously changing.

Kwatz is sold at a low value. Large quantities are purchased. The value of each watch is almost constant.

QUESTION 4

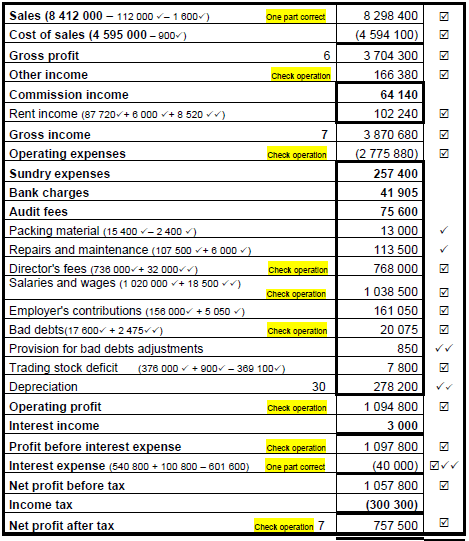

4.1 MUSICA LIMITED

INCOME STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2015

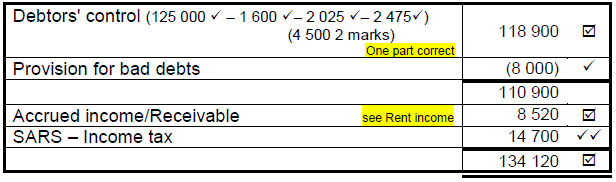

4.1 TRADE AND OTHER RECEIVABLES

4.3 AUDIT REPORT

4.3.1 The audit report is an example of a/an (qualified/unqualified/disclaimer of opinion) audit report.

Disclaimer of opinion√

4.3.2 Who is the audit report addressed to? Give a reason for your answer.

Shareholders√

They are the owners of the company and have appointed the auditors√

4.3.3 Explain why it is likely that this audit report will have a negative effect on the value of the shares of this company on the JSE.

Any valid explanation√√

- The value of the shares will decrease

- Shareholders lose confidence in the company and might sell their shares

- Potential shareholders would not want to invest in this company

QUESTION 5

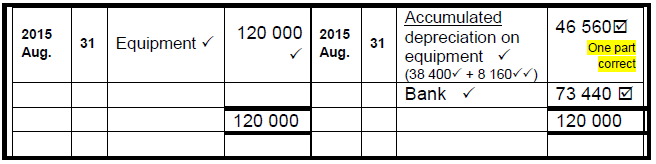

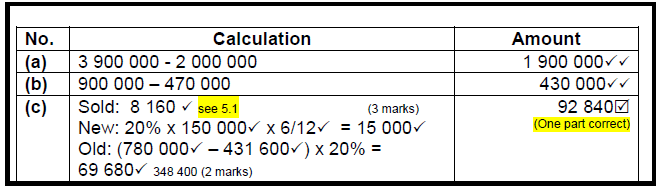

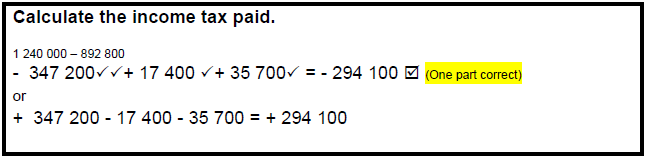

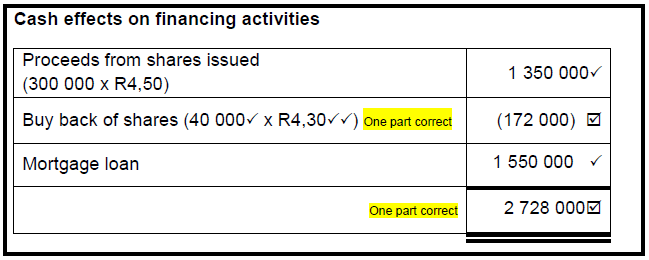

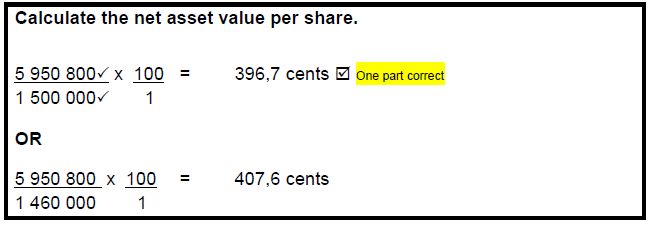

5.1 ASSET DISPOSAL

5.2

5.3.1

5.3.2

5.4

5.5.1

5.5.2

5.5.3

5.6.1 The directors are not satisfied with the liquidity position. Quote and explain THREE relevant financial indicators (with figures) to support this statement.

- Current ratio increased from 1,8 : 1 in 2015 to 3,3 : 1 in 2016

- Acid test ratio increased from 1,2 : 1 in 2015 to 1,6 : 1 in 2016

- The stock turnover rate declined from 5 times in 2015 to 3 times in 2016

Do not accept Debtors' Collection and Creditors' Payment Period

5.6.2 The directors decided to increase the loan during the current financial year. Explain why this was a good decision. Quote and explain TWO financial indicators (with figures) in your answer.

Ratio √√

Figures and trend √√

Comment beyond trend √√ √√

ROTCE

- This has increased from 21,2% to 24,2%

- Positively geared as ROTCE is higher than interest rate (10,5%)

DEBT-EQUITY RATIO

- This has increased from 0,09 : 1 to 0,33 : 1 see 5.5.3

- Low financial risk/not making much use of loans. Relies more on own funds

5.6.3 The directors were pleased with the price that the company paid to buy back the 40 000 shares. Give a suitable reason why the directors felt that way. Quote relevant financial indicators (with figures) to support your answer.

Reason √√

Relevant figure √

Paid R4,30 per share to buy back shares. This is lower than the market value per share (2015 – 480 cents; 2016 – 505 cents).

(not a big difference to the NAV – 362 cents and 408 cents)

Average issue price was R3,70.

Purchased at a lower price than the issue price of the additional shares. (R4,50)

QUESTION 6

6.1 KOBUS HARDWARE

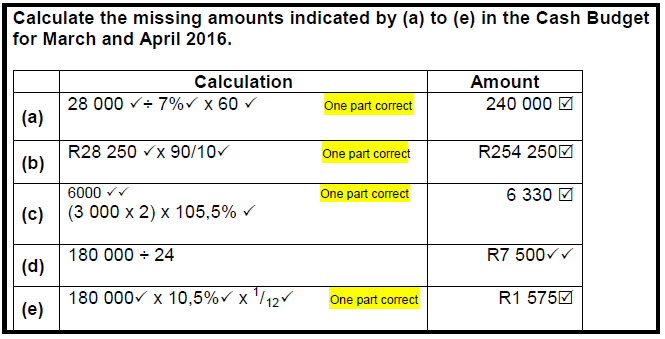

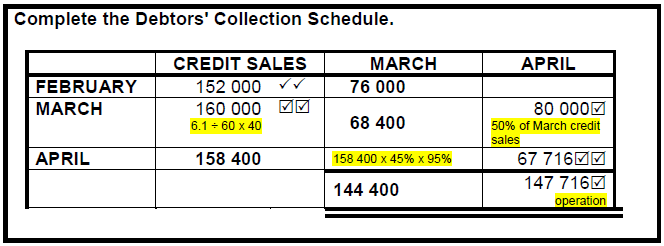

6.1.1

6.1.2

6.1.3

6.1.4 The Cash Budget for March and April 2016 indicates that this business will face serious financial difficulties. Identify TWO items to support this statement. Quote relevant figures.

Item √√ Figures √√

- The overdraft in March is R75 300 and April is R44 900. (This exceeds the overdraft limit of R40 000 as approved by bank.)

- The business is going to acquire a loan of R180 000 in April 2016.

6.1.5 Explain why each of the items reflects a problem for the business and advise Kobus regarding each case.

| Item | Explanation |

| Collection from debtors | Any two valid reasons √√ Alternative valid answers acceptable • Collections are much lower than expected. • This will cause a cash flow problem. • Internal control of debtors is poor. |

| Payments to creditors | Any two valid reasons √√ Alternative valid answers acceptable • These are a lot lower than they should have been. • Suppliers will stop selling to the business. • Interest can be charged by the creditors. • Poor credit rating for the business. |

| Insurance | Any two valid reasons √√ Alternative valid answers acceptable • The policy will lapse (risk of being uninsured). • It will be difficult to replace assets. • There could be an increase in premiums in future. |

| Drawings | Any two valid reasons √√ Alternative valid answers acceptable • This puts strain on meeting more important business expenses. |

6.2 MANAGEMENT OF FIXED ASSETS

Identify ONE problem regarding each vehicle/driver. Quote figures to support your answers. Give Kobus ONE point of advice for EACH problem identified.

| Problem with figures Problem √ √ √ Figures √ √ √ | Advice √ √ √ | |

| Vehicle 1 (Leroy) | Leroy was absent for 8 days./ He is the highest paid driver, R8 000 where other drivers earn R5 000. | Investigate the reason for his absence./Only pay for the number of days at work. |

| Vehicle 2 (Fred) | Fred is travelling too many kilometres (4 600 km for 80 trips = 58 km per trip) which is higher than the maximum of 40 km per customer./He is travelling more km than Bheki (4 200 compared to 2 800 km) but doing fewer trips (70 compared to 110). | Possible disciplinary action against Fred for unauthorised use of vehicle./Improve internal control over the use of the vehicles. |

| Vehicle 3 (Bheki) | Bheki is doing the most number of trips (120) but his vehicle is the oldest and the most expensive to run (R0,81 per km). | Consider replacing this vehicle as it is expensive to maintain. |