Economics Paper 2 Questions - Grade 12 June 2021 Exemplars

Share via Whatsapp Join our WhatsApp Group Join our Telegram GroupINSTRUCTIONS AND INFORMATION

- Answer FOUR questions as follows in the ANSWER BOOK:

SECTION A: COMPULSORY

SECTION B: Answer TWO of the three questions.

SECTION C: Answer ONE of the two questions. - Answer only the required number of questions. Answers in excess of the required number will NOT be marked.

- Answer the questions in full sentences and the format, content and context of your responses must comply with the cognitive requirements of the questions.

- Number the answers correctly according to the numbering system used in this question paper.

- Write the question number above each answer.

- Read ALL the questions carefully.

- Start EACH question on a NEW page.

- Leave 2–3 lines between subsections of questions.

- Use only black or blue ink.

- You may use a non-programmable pocket calculator.

- Write neatly and legibly.

QUESTIONS

SECTION A (COMPULSORY)

QUESTION 1 30 MARKS – 20 MINUTES

1.1 Various options are provided as possible answers to the following questions. Choose the correct answer and write only the letter (A–D) next to the question number (1.1.1–1.1.8) in the ANSWER BOOK, for example 1.1.9 D.

1.1.1 The only option open to perfectly competitive firms to increase profit is to …

- increase the price.

- increase output.

- decrease output.

- decrease the price.

1.1.2 A firm cannot recover … costs should it leave a industry.

- sunk

- variable

- fixed

- total

1.1.3 Barriers of entry make it … for a firm to enter an industry.

- expensive

- cheaper

- easier

- less costly

1.1.4 Products produced by monopolistic competitive firms are …

- unique.

- homogeneous.

- the same.

- differentiated.

1.1.5 The demand curve of a monopolist is also the … curve.

- marginal cost

- marginal revenue

- average revenue

- average cost

1.1.6 In a duopoly there are … oligopolies.

- few

- two

- three

- four

1.1.7 Street lights is an example of a … good.

- demerit

- private

- collective

- community

1.1.8 Private benefits are also known as … benefits.

- social

- external

- internal

- long term (8 x 2) (16)

1.2 Choose a description in COLUMN B that matches an item in COLUMN A. Write only the letter (A–I) next to the question number (1.2.1–1.2.8) in the ANSWER BOOK, for example 1.2.9 J.

COLUMN A | COLUMN B | ||

1.2.1 | Market price | A | Eskom is an example |

1.2.2 | Production costs | B | enjoy the product without paying for it |

1.2.3 | Free riders | C | has a hybrid structure |

1.2.4 | Monopoly | D | determined by the interaction of demand and supply |

1.2.5 | Minimum prices | E | done by means of marketing campaigns and further product variation |

1.2.6 | Non-price competition | F | ability of the buyer or seller to influence the price |

1.2.7 | Monopolistic competition | G | incurred by a business when manufacturing goods |

1.2.8 | Market power | H | enable producers to make a comfortable profit |

I | all factors of production are fixed | ||

(8 x 1) (8)

1.3 Give ONE term for each of the following descriptions. Write only the term next to the question number (1.3.1–1.3.6) in the ANSWER BOOK.

1.3.1 Value of inputs owned by an entrepreneur and used in the total production

1.3.2 A point at which the revenue of a firm selling its product is just enough to cover all costs

1.3.3 Firms that determine their own prices

1.3.4 The benefits to society often not calculated by the individual

1.3.5 Different businesses that produce or supply the same product

1.3.6 Goods that are harmful to the community (6 x 1) (6)

TOTAL SECTION A: 30

SECTION B

Answer any TWO of the three questions from this section in the ANSWER BOOK.

QUESTION 2: MICROECONOMICS 40 MARKS – 30 MINUTES

2.1 Answer the following questions.

2.1.1 List TWO elements of social costs. (2)

2.1.2 Why does a monopolistic competitive firm make normal profit in the long run? (2)

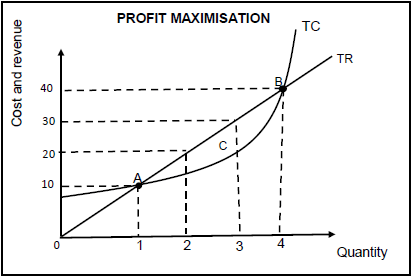

2.2 Study the graph below and answer the questions that follow.

2.2.1 In which market structure does the graph above belong? (1)

2.2.2 What does area ACB represent? (1)

2.2.3 Briefly describe the term profit. (2)

2.2.4 Explain why profit is maximised at quantity 3. (2)

2.2.5 Why does the TC curve not start at zero like the TR curve? (2 x 2) (4)

2.3 Study the extract below and answer the questions that follow.

MONOPOLY IN THE SHORT RUN There are natural and artificial monopolies. In the short-run, a monopolist firm cannot vary all its factors of production as its cost curves are similar to a firm operating in perfect competition. Also, in the short-run a monopolist might incur losses. [Adapted from www.toppr.com.guides] |

2.3.1 Give an appropriate term for costs that change with production. (1)

2.3.2 Give ONE reason for the existence of a natural monopoly. (1)

2.3.3 Briefly describe the term artificial monopoly. (2)

2.3.4 Why will it not benefit a monopolist to charge very high prices? (2)

2.3.5 Draw the graph of an economic loss in the monopoly. (4)

2.4 Differentiate between productive efficiency and allocative efficiency. (2 x 4) (8)

2.5 Why is a cost benefit analysis necessary for public projects? (4 x 2) (8)

[40]

QUESTION 3: MICROECONOMICS 40 MARKS – 30 MINUTES

3.1 Answer the following questions.

3.1.1 List TWO markets that are close to being perfect markets. (2)

3.1.2 How is immobility of labour a cause of market failure? (2)

3.2 Study the table below and answer the questions that follow.

COST AND REVENUE TABLE

|

3.2.1 At which unit is profit maximised? (1)

3.2.2 Determine the marginal cost for A in the table above. (1)

3.2.3 Briefly explain the concept average cost. (2)

3.2.4 Why is price equal to average revenue? (2)

3.2.5 With reference to the table above draw a total revenue curve. (4)

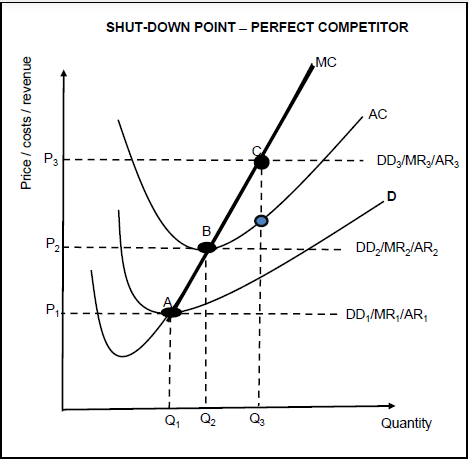

3.3 Study the graph below and answer the questions that follow.

3.3.1 Provide a correct label for curve D. (1)

3.3.2 Identify a shut-down point from the graph above. (1)

3.3.3 Briefly describe the term marginal revenue. (2)

3.3.4 Why is the perfect competitor making economic profit at P3? (2)

3.3.5 With reference to the above graph, explain how the supply curve of a perfect competitor is determined. (2 x 2) (4)

3.4 Compare the monopoly and perfect market in terms of the nature of products they produce. (2 x 4) (8)

3.5 How can the existence of perfect markets impact on consumers and producers? (8)

[40]

QUESTION 4: MICROECONOMICS 40 MARKS – 30 MINUTES

4.1 Answer the following questions.

4.1.1 List TWO barriers to entry into an artificial monopoly. (2)

4.1.2 Why is collusion not possible under perfect competition? (2)

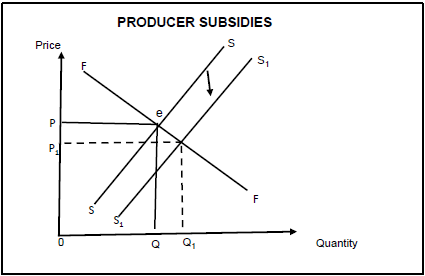

4.2 Study the graph below and answer the questions that follow.

4.2.1 What causes the shift of the supply curve from SS to S1 S1? (1)

4.2.2 Provide a suitable name for curve FF. (1)

4.2.3 Briefly describe the term subsidy. (2)

4.2.4 Briefly explain the purpose of levying taxes. (2)

4.2.5 With reference to the graph above, explain the effect of producer subsidies. (2 x 2) (4)

4.3 Study the information below and answer the questions that follow.

COMPETITION WATCHDOG HALTS TAKEOVER German company Aton’s acquisition of engineering firm Murray & Roberts hit an obstacle as competition regulators believe the transaction is anti- competitive. [Adapted from fin24 pm, 19/07/19] |

4.3.1 Identify the role of the Competition Commission as addressed in the extract. (1)

4.3.2 To whom does the Competition Commission make its recommendations? (1)

4.3.3 Briefly describe the term merger as used in economics. (2)

4.3.4 Briefly explain the objective of a competition policy. (2)

4.3.5 Why is competition in the market good for the economy? (2 x 2) (4)

4.4 With the aid of industry and individual producer graphs, explain how the long-run equilibrium in a perfect market will be achieved when an economic loss was made in the short run. (8)

4.5 Examine the importance of branding and advertising in a monopolistic competitive industry. (8)

[40]

TOTAL SECTION B: 80

SECTION C

Answer any ONE of the two questions from this section in the ANSWER BOOK. Your answer will be assessed as follows:

STRUCTURE OF THE ESSAY | MARK ALLOCATION |

Introduction

| Max. 2 |

Body | Max. 26 |

Additional part: Give own opinion/Critically discuss/Evaluate/Critically evaluate/Draw a graph and explain/Use the graph given and explain/Complete the given graph/Calculate/Deduce/Compare/Explain/ Distinguish/Interpret/Briefly debate | Max. 10 |

Conclusion

| Max. 2 |

TOTAL | 40 |

QUESTION 5: MICROECONOMICS 40 MARKS – 40 MINUTES

- Examine in detail, oligopoly as a market structure under the following headings

- Collusion (13)

- Prices and production levels (13) (26 marks)

- Why do oligopolies often collude, although it is illegal in South Africa? (10 marks) [40]

QUESTION 6: MICROECONOMICS 40 MARKS – 40 MINUTES

- Discuss in detail, state intervention as a consequence of market failure under the following headings:

- Direct control (6)

- Imperfect market (8)

- Government involvement in production (12) (26 marks)

- Justify the implementation of minimum wages by the government. (10 marks) [40]

TOTAL SECTION C: 40

GRAND TOTAL: 150