Economics Paper 2 Memorandum - Grade 12 June 2021 Exemplars

Share via Whatsapp Join our WhatsApp Group Join our Telegram GroupMEMORANDUM

SECTION A (COMPULSORY)

QUESTION 1

1.1 MULTIPLE-CHOICE QUESTIONS

1.1.1 B ?? increase output

1.1.2 A ?? sunk

1.1.3 A ?? expensive

1.1.4 D ?? differentiated

1.1.5 C ?? average revenue

1.1.6 B ?? two

1.1.7 D ?? community

1.1.8 C ?? internal (8 x 2) (16)

1.2 MATCHING ITEMS

1.2.1 D ? determined by the interaction of demand and supply

1.2.2 G ? incurred by a business when manufacturing a good

1.2.3 B ? enjoy the product without paying for it

1.2.4 A ? Eskom is an example

1.2.5 H ? enable producers to make a comfortable profit

1.2.6 E ? done by means of marketing campaigns and further product variation

1.2.7 C ? has a hybrid structure

1.2.8 F ? ability of the buyer or seller to influence the price (8 x 1) (8)

1.3 GIVE ONE TERM

1.3.1 Implicit cost ?

1.3.2 Break-even point/normal profit ?

1.3.3 Price makers/price setters ?

1.3.4 Positive externality ?/external benefit

1.3.5 Industry ?

1.3.6 Demerit goods ? (6 x 1) (6)

TOTAL SECTION A: 30

SECTION B

Answer any TWO of the three questions from this section in the ANSWER BOOK.

QUESTION 2

2.1 Answer the following questions.

2.1.1 List TWO elements of social costs.

- Private costs ?

- External costs ? (2)

2.1.2 Why does a monopolistic competitive firm make normal profit in the long run?

- Economic profit in the short run attracts more firms to enter the market thereby leading to economic profit diminishing and firms make normal profit. ??

(Accept any relevant correct response.) (2)

2.2

2.2.1 In which market structure does the graph above belong?

- Perfect market ? (1)

2.2.2 What does area ACB represent?

- Profit area ? (1)

2.2.3 Briefly describe the term profit.

- Profit is the positive difference between total revenue and total cost ?? / Profit = TR – TC

- Profit is the remuneration for the entrepreneur ??

(Accept any other correct and relevant response.) (2)

2.2.4 Explain why profit is maximised at quantity 3.

- Profit is maximised at quantity 3 because it is where the difference between TR and TC is the largest. ?? (2)

2.2.5 Why does the TC curve not start at zero like the TR curve?

- Total cost is the sum of fixed cost and variable cost while total revenue is price multiply by quantity. ??

- Fixed costs are cost paid irrespective of the level of production; therefore, the firm pays costs even if production is zero. ??

- Total revenue starts at zero because when there are no units sold revenue is zero. ??

(Accept any other correct relevant response.) (2 x 2) (4)

2.3 DATA RESPONSE

2.3.1 Give an appropriate term for costs that change with production.

- Variable costs ? (1)

2.3.2 Give ONE reason for the existence of a natural monopoly.

- High development costs ?

- Access to a resource / only owner of natural resource ?

(Accept any other correct relevant response.) (1)

2.3.3 Briefly describe term artificial monopoly.

- Artificial monopoly is a monopoly where barriers to entry are not economic in nature, such as a patent. ??

(Accept any other correct relevant response.) (2)

2.3.4 Why will it not benefit a monopolist to charge very high prices?

- Consumers will buy alternate products due to budget constraints ??

- The total revenue will decline because the demand will decrease ??

- Loss of revenue could compromise the efficiency of the business operation ??

- It might lead to closing the operation due to loss in market share / income ?? (2)

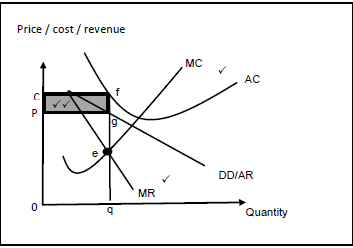

2.3.5 Draw the graph of an economic loss in the monopoly.

Mark allocation

- Correct drawing, labelling and position of cost curves = 1 mark

- Correct drawing, labelling and positioning of revenue curves = 1 mark

- Correct indication of economic loss = 2 marks

Max. 4 marks (4)

2.4 Differentiate between productive efficiency and allocative efficiency.

Productive efficiency

- A situation in which an economy is able to produce goods and services at the lowest possible average cost ??

- Productive efficiency enables society to have a better trade-off and enable people to consume more goods and services ??

- It is shown on the production possibility curve where all points on the curve are productively efficient ??

(Accept any other correct relevant response.) Max. 4

Allocative efficiency

- A situation where firms in an industry use the available resources to produce the output most demanded by consumers ??

- The goods produced reflect consumers’ tastes ??

- Resources are allocated in the right proportions ??

- This applies to perfect competition in the long run ??

(Accept any other correct relevant response.) Max. 4 (8)

2.5 Why is a cost benefit analysis necessary for public projects?

- CBA leads to objective decision-making by weighing up costs and benefits ??

- CBA is applied to those projects where it is expected there will be a significant difference between social costs and benefits, in other words a likelihood of market failure ??

- It includes the wider social impact and externalities in the decision- making process ??

- It is used to make final decisions about whether the project should proceed or not ??

- There is an absence of market signals to support whether the project can go ahead or not ??

(Accept any correct relevant response.) (4 x 2) (8)

[40]

QUESTION 3: MICROECONOMICS

3.1

3.1.1 List TWO markets that are close to being perfect markets.

- Stock exchange market

- Foreign exchange market

- Agricultural produced goods market

(Accept any other relevant correct response.) (2 x 1) (2)

3.1.2 How is immobility of labour a cause of market failure?

- It takes time for labour to move into a new occupation because of the training needed

- Movement from one place to another is not free and may be very costly

(Accept any other relevant correct response.) (1 x 2) (2)

3.2 DATA RESPONSE

3.2.1 At which unit is profit maximised?

- Unit 2 (1)

3.2.2 Determine the marginal cost for A in the table above.

- 11 (1)

3.2.3 Briefly explain the concept average cost.

- Average cost is the cost of producing one unit/cost per unit (2)

3.2.4 Why is price equal to average revenue?

- Average revenue is revenue per unit and is calculated by dividing total revenue by number of units which is then the price.

(Accept any other relevant correct response.) (2)

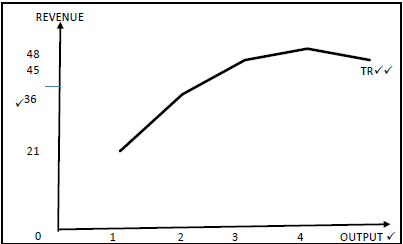

3.2.5 With reference to the table above draw a total revenue curve.

Mark allocation

- Labelling of axes = 1 mark

- Labelling on the axes = 1 mark

- Correct labelling and shape of total revenue curve = 2 marks

Max. = 4 marks (4)

3.3 DATA RESPONSE

3.3.1 Provide a correct label for curve D.

- Average variable cost / AVC (1)

3.3.2 Identify a shut-down point from the graph above.

- Point A (1)

3.3.3 Briefly describe the term marginal revenue.

- Marginal revenue is the additional revenue received from selling an additional unit.

(Accept any other correct relevant response.) (2)

3.3.4 Why is the perfect competitor making economic profit at P3?

- Economic profit is made at P3, because average revenue is greater than average cost

(Accept any other correct relevant response.) (2)

3.3.5 With reference to the above graph, explain how the supply curve of a perfect competitor is determined.

- The supply curve of a perfect competitor is determined by the rising part of the business’s marginal cost curve above the minimum of its average variable cost curve

- The supply curve of the perfect competitor in the graph starts from point A and slopes upward from there

- The reason for the upward slope is because the marginal cost increases as output increases

(Accept any other correct relevant response.) (2 x 2) (4)

3.4 Compare the monopoly and perfect market in terms of the nature of products they produce.

Perfect market

- All products sold in the perfect market are homogeneous

- All these products are exactly the same regarding quality and appearance

- It makes no difference to a buyer where and from whom he or she buys the product

Max. 4

Monopoly

- Products sold in a monopoly are unique

- There are no close substitutes that buyers can turn to

- It is therefore not possible for another firm to enter the market with a similar product and compete with the existing monopoly

(Accept any other correct relevant response.)

Max. 4

(8)

3.5 How could the existence of perfect markets impact on the consumers and producers?

Consumers Positive

- Consumers can benefit from perfect competition because they will be paying low prices for high quality of goods and services

Negative

- Consumers may not be happy with identical products – it kills the uniqueness of an individual

- There will be no choice on the products to consume

(Accept any other relevant correct response.)

Max. 4

Producers Positive

- Profit maximisation at the lower average cost

- No discrimination among firms since the products are homogeneous and prices are the same

Negative

- Does not benefit the firm to adjust the price according to the firm’s needs

- Cannot make economic profit in the long run

(Accept any other relevant correct response.)

Max. 4

(8)

[40]

QUESTION 4: MICROECONOMICS

4.1

4.1.1 List TWO barriers to entry into an artificial monopoly.

- Patents ?

- Licences ?

(Accept any other relevant correct response.) (2)

4.1.2 Why is collusion not possible under perfect competition?

- There are many firms who are too insignificant to influence the market. ??

(Accept any other relevant correct response.) (2)

4.2 DATA RESPONSE

4.2.1 What causes the shift of the supply curve from SS to S1S1?

- The introduction of a subsidy ? (1)

4.2.2 Provide a suitable name for curve FF.

- Demand curve ? (1)

4.2.3 Briefly describe the term subsidy.

- Financial assistance given by the government to producers to lower the cost of production. ??

(Accept any other relevant correct response.) (2)

4.2.4 Briefly explain the purpose of levying taxes.

- To attempt recovery of the external cost ??

- To provide revenue for the state ??

(Accept any other relevant correct response.) (2)

4.2.5 With reference to the graph above, explain the effect of producer subsidies.

- FF and SS are the original demand and supply curves intersecting at equilibrium point ‘e’, with equilibrium price P and quantity Q. ??

- The introduction of a subsidy causes an increase in supply from SS to S1S1, thereby leading to a decrease in equilibrium price to P1 and an increase in quantity to Q1. ??

- The cost of production decreases and quantity increases. ??

(Accept any other relevant correct response.) (2 x 2) (4)

4.3 DATA RESPONSE

4.3.1 Identify the role of the Competition Commission addressed in the extract.

- Disallowing mergers and acquisitions to go ahead ? (1)

4.3.2 To whom does the Competition Commission makes its recommendations?

- Competition Tribunal ? (1)

4.3.3 Briefly describe the term merger as used in economics.

- Union of two or more firms to form a single firm ??

(Accept any other relevant correct response.) (2)

4.3.4 Briefly explain the objective of a competition policy.

- Prevent abuse of economic power ??

- Regulate the growth of market power ??

- Prevent restrictive practices especially by oligopolies ??

(Accept any relevant correct response.) (2)

4.3.5 Why is competition in the market good for the economy?

- Consumers get good prices and good quality products ??

- Competition encourages firms to invent low-cost manufacturing processes which can increase profits ??

- Competition encourages businesses to conduct a consumer need analysis in order to meet their needs ??

- Competition can lead to higher productivity and efficiency in the market ??

(Accept any other relevant correct response.) (2 x 2) (4)

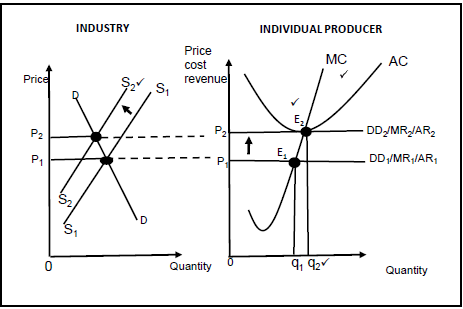

4.4 With the aid of industry and individual producer graphs. explain how the long-run equilibrium in a perfect market will be achieved when an economic loss was made in the short run.

Mark allocation

- Decrease in supply = 1 mark

- Increase in quantity = 1 mark

- New equilibrium point = 1 mark Correct labelling and position of MC and AC = 1 mark

4 marks

- Economic loss in the short run lead to firm exiting the industry, thereby leading to a decrease in supply (supply shifting from S1S1 to S2S2 ) as a result the price rises to P2.

- Individual firms will then take P2 and the higher price will reduce the loss until the price (average revenue) is equal to average cost.

- Supply will continue to decrease until the remaining firms make at least normal profit and there will be no incentive for firms to leave the industry.

- Firms will then make normal profit at P2 and higher quantity at q2.

(Accept any other relevant correct response.)

Max. 4 (8)

4.5 Examine the importance of branding and advertising in a monopolistic competitive industry.

- Branding and advertising are important to a monopolistically competitive firm because they are the best way to differentiate it from its competitors.

- Brands facilitates easy identification of the products by consumers and thereby increasing sales.

- In order for the firms to maintain the reputation of the brand, they produce high-quality products because it takes one bad experience to ruin the value of the brand.

- A brand and its reputation are built on the firm’s effective advertising campaign.

- Advertising is valuable to society because it helps inform consumers and markets work best when consumers are well informed.

- Advertising and brands can help minimise the costs of choosing between different products because of consumers’ familiarity with the firms and their quality.

- Advertising allows new firms to enter into a market.

- Consumers might be hesitant to purchase products with which they are unfamiliar. Advertising can educate and inform those consumers, making them comfortable enough to give those products a try.

(Accept any other correct relevant response.)

(4 x 2) (8)

[40]

TOTAL SECTION B: 80

SECTION C

Answer ONE of the two questions from this section in the ANSWER BOOK.

QUESTION 5

- Examine in detail, oligopoly as a market structure under the following headings

- Collusion (13)

- Prices and production levels (13)

(26 marks)

- Why do oligopolies often collude although it is illegal in South Africa?(10 marks)

[40]

INTRODUCTION

An oligopoly is a market structure dominated by a few producers, each of which has some control over the market.

(Accept any other relevant introduction.) (2)

MAIN PART

Collusion

- Collusion takes place when rival firms cooperate by raising prices and by restricting production in order to maximise their profits.

- Firms often cooperate instead of competing with one another.

- Collusion can take two forms, cartels and price leadership

Cartels

- Collusion occurs openly and formally.

- Is also referred to as overt /explicit collusion.

- A cartel is a group of producers whose goal is to form a collective monopoly in order to fix prices and limit supply and competition.

- Collusion is illegal in South Africa, and is liable to large fines by the Competition Commission.

Price Leadership

- At times collusion can be in the form of price leadership, which is an unspoken agreement among firms.

- Price leadership (tacit/implicit collusion) involves one firm serving as a price leader while another follow.

- While the price leader changes its price the other do the same.

(Accept any other relevant correct response.)

Max. 13

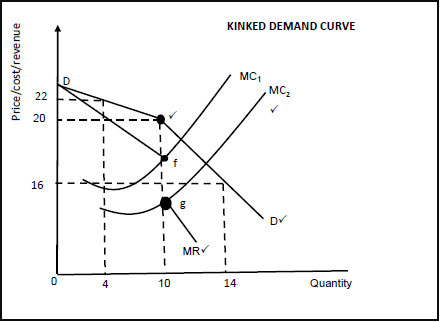

Prices and production levels

- It is difficult to draw the demand curve, marginal revenue curve and marginal cost curve, because oligopolist take into account the reaction of its rivals

- A kinked demand curve is used to explain prices and quantities in oligopoly markets.

- This demand curve consists of two sections – the top section that relates to high prices has a very elastic slope and the bottom section that relates to lower prices has very inelastic slope.

- This model is based on the assumption that each business believes that if it raises its prices, others will not follow but if it cuts its prices other businesses will cut their prices.

Mark allocation

- Correct drawing and labelling of kinked demand curve = 1 mark

- Indication of Kink in the demand curve = 1 mark

- Correct drawing and labelling marginal cost curves = 1 mark

- Marginal revenue curve = 1 mark

Max. 4 marks

- If the oligopolist wants to increase its profit by increasing the price to R22, the quantity demanded will fall to 4 unit, then total revenue fall to R88. ??

- Other oligopolists will not follow the lead, the firm that increases the price will lose its customers to those that did not increase the price. ??

- If the oligopolist reduces the price from R20 to R16, output will increase to 14 units and total revenue to R224. ?? Other firms will feel forced to cut their prices because they will lose customers if they do not. ??

- The oligopolist will produce where MR=MC, at price R20 and quantity 10. ??

- This confirms that prices in an oligopoly are rigid. ?? Max. 13

(Accept any other correct relevant response.) (26)

ADDITIONAL PART

Collusion between oligopolies occur because:

- it is an effort to reduce uncertainty – they can enjoy the advantage of higher profit and limit other businesses to enter the market (to control the market / to form a collective monopoly) ??

- the cost of doing business in an oligopoly market is very high, that is why these firms use non-price competition such as advertising, and this can cost a very large amount of money ??

- firms are mutually interdependent and large amounts of money is often required to monitor one another’s actions ??

- it increases the firms’ total cost of doing business ??

- this often makes firms to engage in cooperation with one another instead of competing even though it is illegal in South Africa ??

(Accept any other relevant correct response.) (5 x 2) (10)

CONCLUSION

There is an element of interdependency in an oligopoly as the decisions taken by each firm in an oligopoly depends on decision taken by each of the other firms. ?? (Accept any other relevant conclusion.) (2)

[40]

QUESTION 6: MICROECONOMICS

- Discuss in detail state intervention as a consequence of market failure under the following headings:

- Direct control (6)

- Imperfect market (8)

- Government involvement in production (12) (26 marks)

- Justify the implementation of minimum wages by the government. (10 marks)

[40]

INTRODUCTION

Market failure means that the best available resources or optimal production outcomes has not been achieved. ??

(Accept any other correct relevant introduction.) (2)

BODY

MAIN PART:

Direct control

- Government can choose to pass laws in an attempt to control and constrain the behaviour of businesses and individuals, who generate negative externalities. ??

- Government often imposes taxes on the production of alcohol and tobacco. ??

These are often called sin taxes. ??

- Advertising by the tobacco industry is prohibited and alcohol may not be sold to persons under the age of 18 years. ??

- The government could require firms to fit anti-pollution equipment that cleans poisonous by-products before they are dumped in rivers. ??

(Accept any other correct relevant response.)

Max. 6

Imperfect markets

Businesses operating in non-competitive markets maximise their profits by supplying less than the optimal quantity of goods or service at a high price ??

The government can deal with the effects of imperfect markets by:

- Taxing the firm’s economic profit ??

- Imposing price controls (maximum prices), thus reducing the firm’s economic profit and ensuring that more people are able to consume the product ??

- Introducing a competition policy to try to increase the level of competition between firms and to make it easier for new firm to enter the industry ??

- In South Africa, the government established the Competition Commission, the Competition Tribunal and the Competition Appeal Court to ensure that the level of competition is not eroded but enhanced ??

- Allowing competition from abroad, through the removal or reduction of tariffs, to restrain the harmful practises of local monopolies ??

(Accept any other correct relevant response.)

Max. 8

Government’s involvement in production

- Governments themselves are involved in producing goods and services ??

- Governments approach to missing markets is to supply the desired goods directly. ?? Taxes are raised to finance the provision of such goods. ??

- Community goods are provided free of charge, for example defence, police and street lighting ??

- Some collective goods are provided for a user fee, such as refuse removal, waste disposal and sewerage drainage. ??

- The provision of some other collective goods is subsidised, for example public transport and clean water ??

- If the macroeconomic objectives of the government are not achieved, that can be perceived as market failure and the government can intervene either on the demand side or supply side ??

- On the demand side, the government can intervene with macroeconomic policies, that is, monetary and fiscal policies ??

- The supply side approach focuses on the capability of the economy and policies that attempt to expand the stock of factors of production and infrastructure to improve the flexibility of factor markets. ??

(Accept any other correct relevant response.)

Max. 12

(26)

ADDITIONAL PART

Justify the implementation of minimum wages by government:

- When government enforces minimum wages, it means workers have to be paid a certain amount and not anything less ??

- The minimum wage is set below equilibrium, leading to a decrease in demand and an increase in supply of labour ??

- The application of minimum wage laws is needed to improve a redistribution of income; ?? to redress inequality (gap between wealthy and poor) ?? and to improve the standard of living for the affected group of labour ??

- Government tried to protect domestic workers and farm workers from exploitation by employees because unskilled labourers cannot negotiate wages ??

- Although minimum wages could lead to increased unemployment because employers are reluctant to employ people at this wage, protection of the employed is justifiable ??

(Accept any other relevant response.) (10)

CONCLUSION

Although the government cannot fulfil the supply of all community goods, there will always be a need to satisfy the aspirations of the entire society. ?? (Accept any other relevant conclusion.) (2)

[40]

TOTAL SECTION C: 40

GRAND TOTAL: 150